绘图函数

该模块的功能允许我们创建图表,以帮助我们快速分析最佳投资组合的属性。 帮助我们快速分析我们的最优投资组合的属性。

下面的例子构建了投资组合和有效边界,并将使用本模块的函数来绘制。 将使用本模块的函数来绘制。

例子

import numpy as np

import pandas as pd

import yfinance as yf

import riskfolio as rp

# Date range

start = '2016-01-01'

end = '2019-12-30'

# Tickers of assets

tickers = ['JCI', 'TGT', 'CMCSA', 'CPB', 'MO', 'APA', 'MMC', 'JPM',

'ZION', 'PSA', 'BAX', 'BMY', 'LUV', 'PCAR', 'TXT', 'TMO',

'DE', 'MSFT', 'HPQ', 'SEE', 'VZ', 'CNP', 'NI', 'T', 'BA']

tickers.sort()

# Downloading the data

data = yf.download(tickers, start = start, end = end)

data = data.loc[:,('Adj Close', slice(None))]

data.columns = tickers

assets = data.pct_change().dropna()

Y = assets

# Creating the Portfolio Object

port = rp.Portfolio(returns=Y)

# To display dataframes values in percentage format

pd.options.display.float_format = '{:.4%}'.format

# Choose the risk measure

rm = 'MSV' # Semi Standard Deviation

# Estimate inputs of the model (historical estimates)

method_mu='hist' # Method to estimate expected returns based on historical data.

method_cov='hist' # Method to estimate covariance matrix based on historical data.

port.assets_stats(method_mu=method_mu, method_cov=method_cov, d=0.94)

# Estimate the portfolio that maximizes the risk adjusted return ratio

w1 = port.optimization(model='Classic', rm=rm, obj='Sharpe', rf=0.0, l=0, hist=True)

# Estimate points in the efficient frontier mean - semi standard deviation

ws = port.efficient_frontier(model='Classic', rm=rm, points=20, rf=0, hist=True)

# Estimate the risk parity portfolio for semi standard deviation

w2 = port.rp_optimization(model='Classic', rm=rm, rf=0, b=None, hist=True)

模块函数

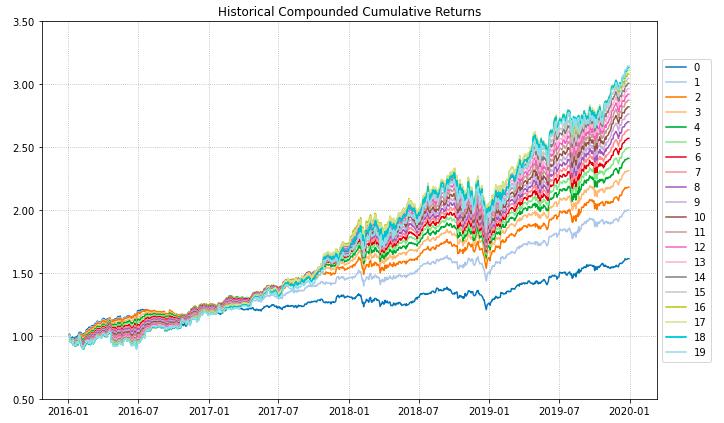

- PlotFunctions.plot_series(returns, w, cmap='tab20', n_colors=20, height=6, width=10, ax=None)[源代码]

Create a chart with the compounded cumulative of the portfolios.

- 参数:

returns (DataFrame) – Assets returns.

w (DataFrame of shape (n_assets, n_portfolios)) – Portfolio weights.

cmap (cmap, optional) – Colorscale used to plot each portfolio compounded cumulative return. The default is ‘tab20’.

n_colors (int, optional) – Number of distinct colors per color cycle. If there are more assets than n_colors, the chart is going to start to repeat the color cycle. The default is 20.

height (float, optional) – Height of the image in inches. The default is 6.

width (float, optional) – Width of the image in inches. The default is 10.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis

示例

ax = rp.plot_series(returns=Y, w=ws, cmap='tab20', height=6, width=10, ax=None)

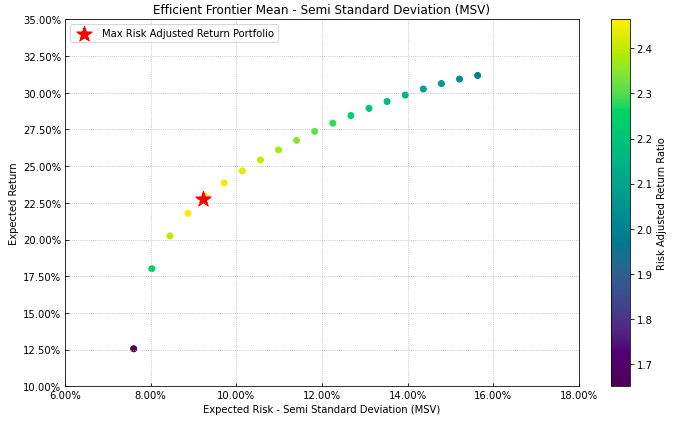

- PlotFunctions.plot_frontier(w_frontier, mu, cov=None, returns=None, rm='MV', kelly=False, rf=0, alpha=0.05, a_sim=100, beta=None, b_sim=None, kappa=0.3, solver=None, cmap='viridis', w=None, label='Portfolio', marker='*', s=16, c='r', height=6, width=10, t_factor=252, ax=None)[源代码]

Creates a plot of the efficient frontier for a risk measure specified by the user.

- 参数:

w_frontier (DataFrame) – Portfolio weights of some points in the efficient frontier.

mu (DataFrame of shape (1, n_assets)) – Vector of expected returns, where n_assets is the number of assets.

cov (DataFrame of shape (n_features, n_features)) – Covariance matrix, where n_features is the number of features.

returns (DataFrame of shape (n_samples, n_features)) – Features matrix, where n_samples is the number of samples and n_features is the number of features.

rm (str, optional) –

The risk measure used to estimate the frontier. The default is ‘MV’. Possible values are:

’MV’: Standard Deviation.

’KT’: Square Root Kurtosis.

’MAD’: Mean Absolute Deviation.

’MSV’: Semi Standard Deviation.

’SKT’: Square Root Semi Kurtosis.

’FLPM’: First Lower Partial Moment (Omega Ratio).

’SLPM’: Second Lower Partial Moment (Sortino Ratio).

’CVaR’: Conditional Value at Risk.

’TG’: Tail Gini.

’EVaR’: Entropic Value at Risk.

’RLVaR’: Relativistic Value at Risk.

’WR’: Worst Realization (Minimax).

’CVRG’: CVaR range of returns.

’TGRG’: Tail Gini range of returns.

’RG’: Range of returns.

’MDD’: Maximum Drawdown of uncompounded returns (Calmar Ratio).

’ADD’: Average Drawdown of uncompounded cumulative returns.

’DaR’: Drawdown at Risk of uncompounded cumulative returns.

’CDaR’: Conditional Drawdown at Risk of uncompounded cumulative returns.

’EDaR’: Entropic Drawdown at Risk of uncompounded cumulative returns.

’RLDaR’: Relativistic Drawdown at Risk of uncompounded cumulative returns.

’UCI’: Ulcer Index of uncompounded cumulative returns.

kelly (bool, optional) – Method used to calculate mean return. Possible values are False for arithmetic mean return and True for mean logarithmic return. The default is False.

rf (float, optional) – Risk free rate or minimum acceptable return. The default is 0.

alpha (float, optional) – Significance level of VaR, CVaR, EVaR, RLVaR, DaR, CDaR, EDaR, RLDaR and Tail Gini of losses. The default is 0.05.

a_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of losses. The default is 100.

beta (float, optional) – Significance level of CVaR and Tail Gini of gains. If None it duplicates alpha value. The default is None.

b_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of gains. If None it duplicates a_sim value. The default is None.

kappa (float, optional) – Deformation parameter of RLVaR and RLDaR, must be between 0 and 1. The default is 0.30.

solver (str, optional) – Solver available for CVXPY that supports power cone programming. Used to calculate RLVaR and RLDaR. The default value is None.

cmap (cmap, optional) – Colorscale that represents the risk adjusted return ratio. The default is ‘viridis’.

w (DataFrame of shape (n_assets, 1), optional) – A portfolio specified by the user. The default is None.

label (str or list, optional) – Name or list of names of portfolios that appear on plot legend. The default is ‘Portfolio’.

marker (str, optional) – Marker of w. The default is “*”.

s (float, optional) – Size of marker. The default is 16.

c (str, optional) – Color of marker. The default is ‘r’.

height (float, optional) – Height of the image in inches. The default is 6.

width (float, optional) – Width of the image in inches. The default is 10.

t_factor (float, optional) –

Factor used to annualize expected return and expected risks for risk measures based on returns (not drawdowns). The default is 252.

\[\begin{split}\begin{align} \text{Annualized Return} & = \text{Return} \, \times \, \text{t_factor} \\ \text{Annualized Risk} & = \text{Risk} \, \times \, \sqrt{\text{t_factor}} \end{align}\end{split}\]ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib Axes

示例

label = 'Max Risk Adjusted Return Portfolio' mu = port.mu cov = port.cov returns = port.returns ax = rp.plot_frontier(w_frontier=ws, mu=mu, cov=cov, returns=returns, rm=rm, rf=0, alpha=0.05, cmap='viridis', w=w1, label=label, marker='*', s=16, c='r', height=6, width=10, t_factor=252, ax=None)

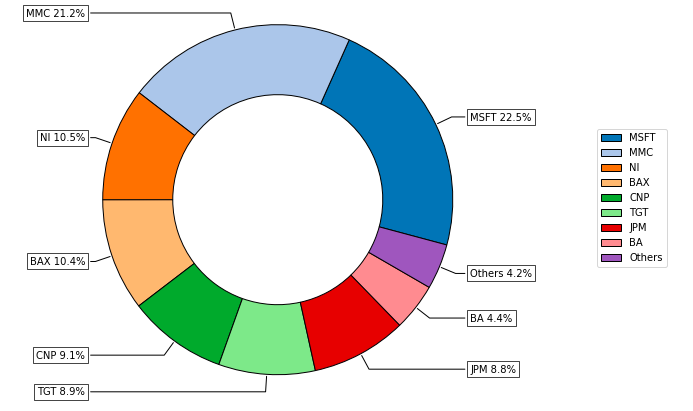

- PlotFunctions.plot_pie(w, title='', others=0.05, nrow=25, cmap='tab20', n_colors=20, height=6, width=8, ax=None)[源代码]

Create a pie chart with portfolio weights.

- 参数:

w (DataFrame of shape (n_assets, 1)) – Portfolio weights.

title (str, optional) – Title of the chart. The default is “”.

others (float, optional) – Percentage of others section. The default is 0.05.

nrow (int, optional) – Number of rows of the legend. The default is 25.

cmap (cmap, optional) – Color scale used to plot each asset weight. The default is ‘tab20’.

n_colors (int, optional) – Number of distinct colors per color cycle. If there are more assets than n_colors, the chart is going to start to repeat the color cycle. The default is 20.

height (float, optional) – Height of the image in inches. The default is 10.

width (float, optional) – Width of the image in inches. The default is 10.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis.

示例

ax = rp.plot_pie(w=w1, title='Portfolio', height=6, width=10, cmap="tab20", ax=None)

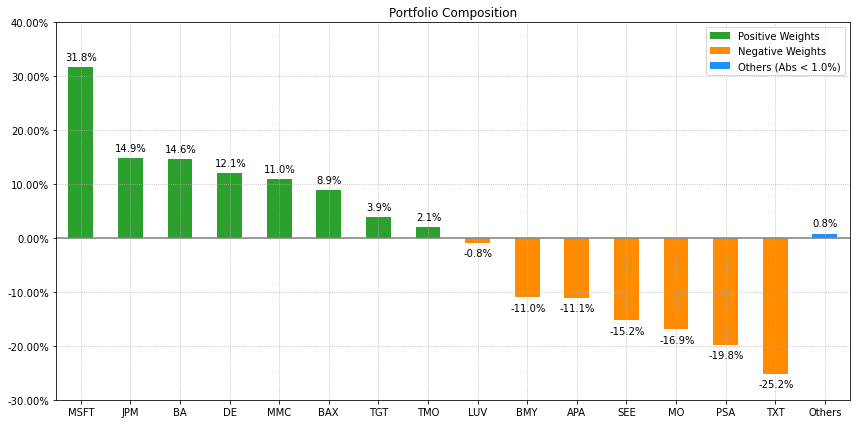

- PlotFunctions.plot_bar(w, title='', kind='v', others=0.05, nrow=25, cpos='tab:green', cneg='darkorange', cothers='dodgerblue', height=6, width=10, ax=None)[源代码]

Create a bar chart with portfolio weights.

- 参数:

w (DataFrame of shape (n_assets, 1)) – Portfolio weights.

title (str, optional) – Title of the chart. The default is “”.

kind (str, optional) – Kind of bar plot, “v” for vertical bars and “h” for horizontal bars. The default is “v”.

others (float, optional) – Percentage of others section. The default is 0.05.

nrow (int, optional) – Max number of bars that be plotted. The default is 25.

cpos (str, optional) – Color for positives weights. The default is ‘tab:green’.

cneg (str, optional) – Color for negatives weights. The default is ‘darkorange’.

cothers (str, optional) – Color for others bar. The default is ‘dodgerblue’.

height (float, optional) – Height of the image in inches. The default is 10.

width (float, optional) – Width of the image in inches. The default is 10.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis.

示例

ax = rp.plot_bar(w, title='Portfolio', kind="v", others=0.05, nrow=25, height=6, width=10, ax=None)

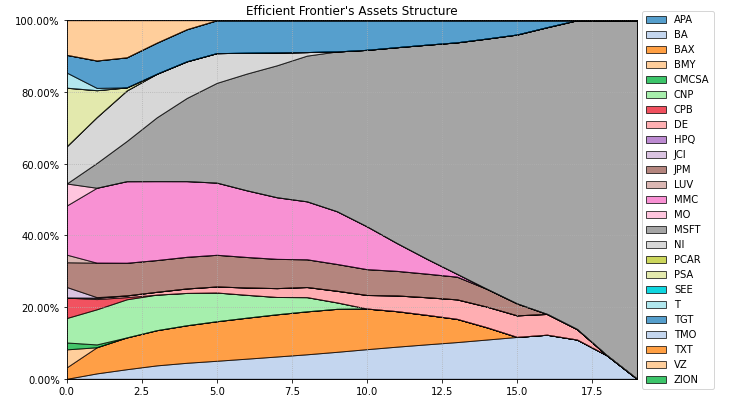

- PlotFunctions.plot_frontier_area(w_frontier, nrow=25, cmap='tab20', n_colors=20, height=6, width=10, ax=None)[源代码]

Create a chart with the asset composition of the efficient frontier.

- 参数:

w_frontier (DataFrame) – Weights of portfolios in the efficient frontier.

nrow (int, optional) – Number of rows of the legend. The default is 25.

cmap (cmap, optional) – Color scale used to plot each asset weight. The default is ‘tab20’.

n_colors (int, optional) – Number of distinct colors per color cycle. If there are more assets than n_colors, the chart is going to start to repeat the color cycle. The default is 20.

height (float, optional) – Height of the image in inches. The default is 6.

width (float, optional) – Width of the image in inches. The default is 10.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis.

示例

ax = rp.plot_frontier_area(w_frontier=ws, cmap="tab20", height=6, width=10, ax=None)

- PlotFunctions.plot_risk_con(w, cov=None, returns=None, rm='MV', rf=0, alpha=0.05, a_sim=100, beta=None, b_sim=None, kappa=0.3, solver=None, percentage=False, erc_line=True, color='tab:blue', erc_linecolor='r', height=6, width=10, t_factor=252, ax=None)[源代码]

Create a chart with the risk contribution per asset of the portfolio.

- 参数:

w (DataFrame of shape (n_assets, 1)) – Portfolio weights.

cov (DataFrame of shape (n_features, n_features)) – Covariance matrix, where n_features is the number of features.

returns (DataFrame of shape (n_samples, n_features)) – Features matrix, where n_samples is the number of samples and n_features is the number of features.

rm (str, optional) –

Risk measure used to estimate risk contribution. The default is ‘MV’. Possible values are:

’MV’: Standard Deviation.

’KT’: Square Root Kurtosis.

’MAD’: Mean Absolute Deviation.

’GMD’: Gini Mean Difference.

’MSV’: Semi Standard Deviation.

’SKT’: Square Root Semi Kurtosis.

’FLPM’: First Lower Partial Moment (Omega Ratio).

’SLPM’: Second Lower Partial Moment (Sortino Ratio).

’CVaR’: Conditional Value at Risk.

’TG’: Tail Gini.

’EVaR’: Entropic Value at Risk.

’RLVaR’: Relativistic Value at Risk.

’WR’: Worst Realization (Minimax).

’CVRG’: CVaR range of returns.

’TGRG’: Tail Gini range of returns.

’RG’: Range of returns.

’MDD’: Maximum Drawdown of uncompounded cumulative returns (Calmar Ratio).

’ADD’: Average Drawdown of uncompounded cumulative returns.

’CDaR’: Conditional Drawdown at Risk of uncompounded cumulative returns.

’EDaR’: Entropic Drawdown at Risk of uncompounded cumulative returns.

’RLDaR’: Relativistic Drawdown at Risk of uncompounded cumulative returns.

’UCI’: Ulcer Index of uncompounded cumulative returns.

rf (float, optional) – Risk free rate or minimum acceptable return. The default is 0.

alpha (float, optional) – Significance level of VaR, CVaR, Tail Gini, EVaR, RLVaR, CDaR, EDaR and RLDaR. The default is 0.05.

a_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of losses. The default is 100.

beta (float, optional) – Significance level of CVaR and Tail Gini of gains. If None it duplicates alpha value. The default is None.

b_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of gains. If None it duplicates a_sim value. The default is None.

kappa (float, optional) – Deformation parameter of RLVaR and RLDaR, must be between 0 and 1. The default is 0.30.

solver (str, optional) – Solver available for CVXPY that supports power cone programming. Used to calculate RLVaR and RLDaR. The default value is None.

percentage (bool, optional) – If risk contribution per asset is expressed as percentage or as a value. The default is False.

erc_line (bool, optional) – If equal risk contribution line is plotted. The default is False.

color (str, optional) – Color used to plot each asset risk contribution. The default is ‘tab:blue’.

erc_linecolor (str, optional) – Color used to plot equal risk contribution line. The default is ‘r’.

height (float, optional) – Height of the image in inches. The default is 6.

width (float, optional) – Width of the image in inches. The default is 10.

t_factor (float, optional) –

Factor used to annualize expected return and expected risks for risk measures based on returns (not drawdowns). The default is 252.

\[\begin{split}\begin{align} \text{Annualized Return} & = \text{Return} \, \times \, \text{t_factor} \\ \text{Annualized Risk} & = \text{Risk} \, \times \, \sqrt{\text{t_factor}} \end{align}\end{split}\]ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis.

示例

ax = rp.plot_risk_con(w=w2, cov=cov, returns=returns, rm=rm, rf=0, alpha=0.05, color="tab:blue", height=6, width=10, t_factor=252, ax=None)

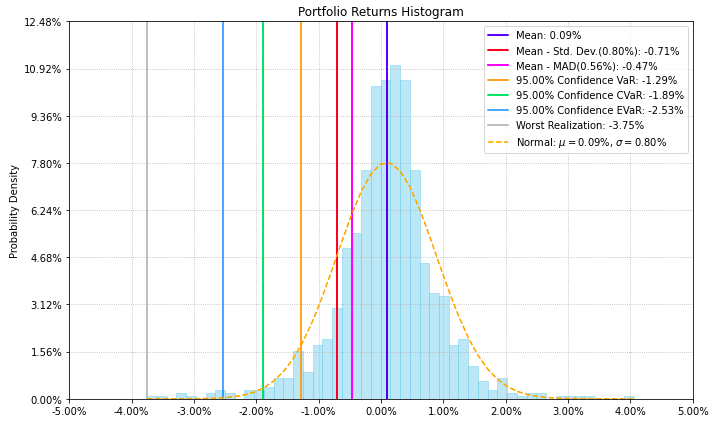

- PlotFunctions.plot_hist(returns, w, alpha=0.05, a_sim=100, kappa=0.3, solver=None, bins=50, height=6, width=10, ax=None)[源代码]

Create a histogram of portfolio returns with the risk measures.

- 参数:

returns (DataFrame) – Assets returns.

w (DataFrame of shape (n_assets, 1)) – Portfolio weights.

alpha (float, optional) – Significance level of VaR, CVaR, EVaR, RLVaR and Tail Gini. The default is 0.05.

a_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of losses. The default is 100.

kappa (float, optional) – Deformation parameter of RLVaR and RLDaR, must be between 0 and 1. The default is 0.30.

solver (str, optional) – Solver available for CVXPY that supports power cone programming. Used to calculate RLVaR and RLDaR. The default value is None.

bins (float, optional) – Number of bins of the histogram. The default is 50.

height (float, optional) – Height of the image in inches. The default is 6.

width (float, optional) – Width of the image in inches. The default is 10.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis.

示例

ax = rp.plot_hist(returns=Y, w=w1, alpha=0.05, bins=50, height=6, width=10, ax=None)

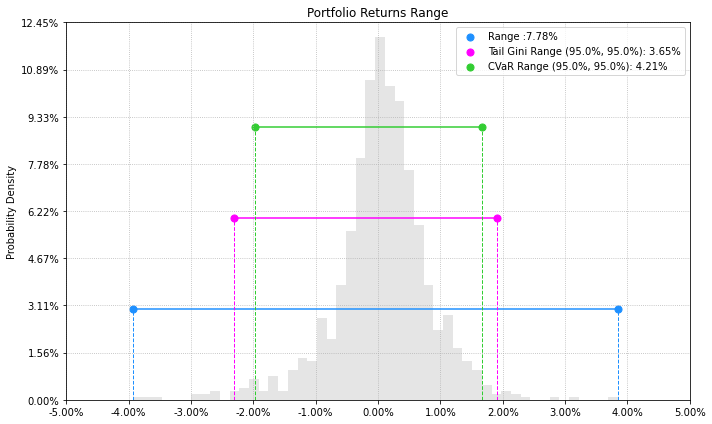

- PlotFunctions.plot_range(returns, w, alpha=0.05, a_sim=100, beta=None, b_sim=None, bins=50, height=6, width=10, ax=None)[源代码]

Create a histogram of portfolio returns with the range risk measures.

- 参数:

returns (DataFrame) – Assets returns.

w (DataFrame of shape (n_assets, 1)) – Portfolio weights.

alpha (float, optional) – Significance level of CVaR and Tail Gini of losses. The default is 0.05.

a_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of losses. The default is 100.

beta (float, optional) – Significance level of CVaR and Tail Gini of gains. If None it duplicates alpha value. The default is None.

b_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of gains. If None it duplicates a_sim value. The default is None.

bins (float, optional) – Number of bins of the histogram. The default is 50.

height (float, optional) – Height of the image in inches. The default is 6.

width (float, optional) – Width of the image in inches. The default is 10.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis.

示例

ax = plot_range(returns=Y, w=w1, alpha=0.05, a_sim=100, beta=None, b_sim=None, bins=50, height=6, width=10, ax=None)

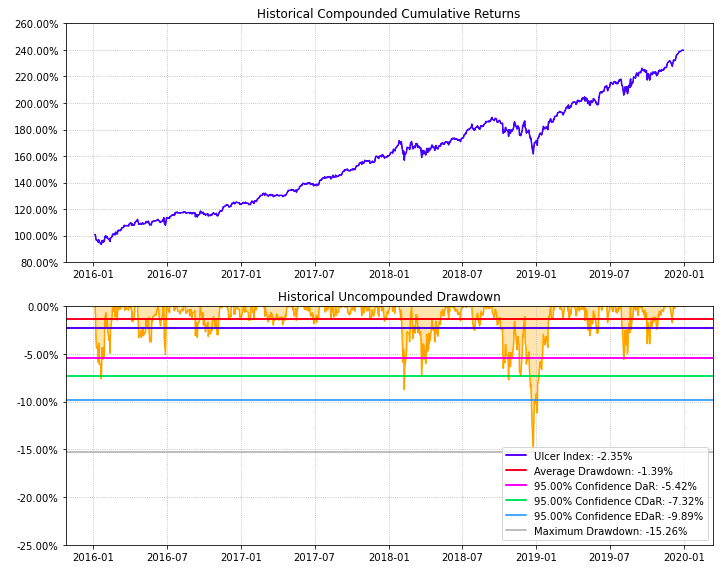

- PlotFunctions.plot_drawdown(returns, w, alpha=0.05, kappa=0.3, solver=None, height=8, width=10, height_ratios=[2, 3], ax=None)[源代码]

Create a chart with the evolution of portfolio prices and drawdown.

- 参数:

returns (DataFrame) – Assets returns.

w (DataFrame, optional) – A portfolio specified by the user. The default is None.

alpha (float, optional) – Significance level of DaR, CDaR, EDaR and RLDaR. The default is 0.05.

kappa (float, optional) – Deformation parameter of RLVaR and RLDaR, must be between 0 and 1. The default is 0.30.

solver (str, optional) – Solver available for CVXPY that supports power cone programming. Used to calculate RLVaR and RLDaR. The default value is None.

height (float, optional) – Height of the image in inches. The default is 8.

width (float, optional) – Width of the image in inches. The default is 10.

height_ratios (list or ndarray) – Defines the relative heights of the rows. Each row gets a relative height of height_ratios[i] / sum(height_ratios). The default value is [2,3].

ax (matplotlib axis of size (2,1), optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the a np.array with Axes objects with plots for further tweaking.

- 返回类型:

np.array

示例

ax = rp.plot_drawdown(returns=Y, w=w1, alpha=0.05, height=8, width=10, ax=None)

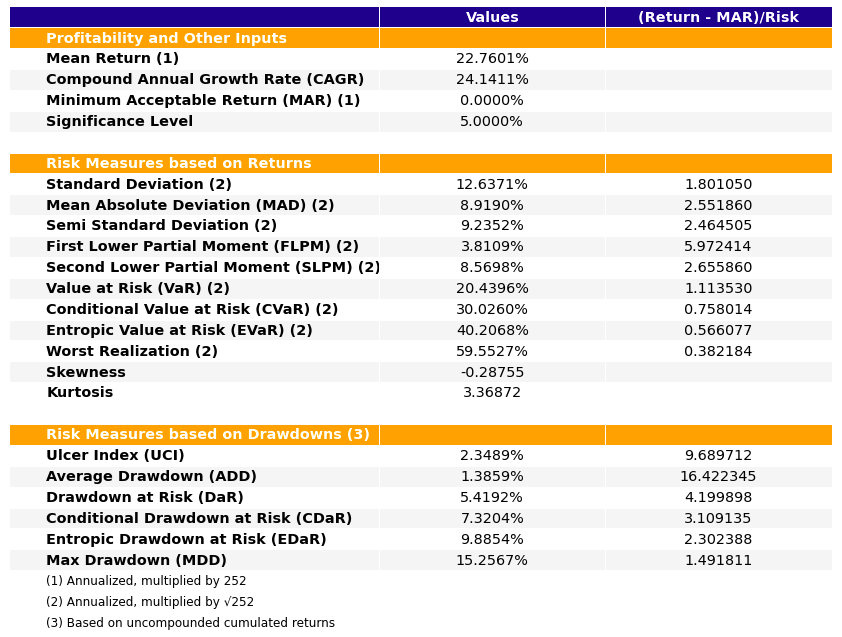

- PlotFunctions.plot_table(returns, w, MAR=0, alpha=0.05, a_sim=100, kappa=0.3, solver=None, height=9, width=12, t_factor=252, ini_days=1, days_per_year=252, ax=None)[源代码]

Create a table with information about risk measures and risk adjusted return ratios.

- 参数:

returns (DataFrame) – Assets returns.

w (DataFrame) – Portfolio weights.

MAR (float, optional) – Minimum acceptable return.

alpha (float, optional) – Significance level of VaR, CVaR, Tail Gini, EVaR, RLVaR, CDaR, EDaR and RLDaR. The default is 0.05.

a_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of losses. The default is 100.

beta (float, optional) – Significance level of CVaR and Tail Gini of gains. If None it duplicates alpha value. The default is None.

b_sim (float, optional) – Number of CVaRs used to approximate Tail Gini of gains. If None it duplicates a_sim value. The default is None.

kappa (float, optional) – Deformation parameter of RLVaR and RLDaR, must be between 0 and 1. The default is 0.30.

solver (str, optional) – Solver available for CVXPY that supports power cone programming. Used to calculate RLVaR and RLDaR. The default value is None.

height (float, optional) – Height of the image in inches. The default is 9.

width (float, optional) – Width of the image in inches. The default is 12.

t_factor (float, optional) –

Factor used to annualize expected return and expected risks for risk measures based on returns (not drawdowns). The default is 252.

\[\begin{split}\begin{align} \text{Annualized Return} & = \text{Return} \, \times \, \text{t_factor} \\ \text{Annualized Risk} & = \text{Risk} \, \times \, \sqrt{\text{t_factor}} \end{align}\end{split}\]ini_days (float, optional) – If provided, it is the number of days of compounding for first return. It is used to calculate Compound Annual Growth Rate (CAGR). This value depend on assumptions used in t_factor, for example if data is monthly you can use 21 (252 days per year) or 30 (360 days per year). The default is 1 for daily returns.

days_per_year (float, optional) – Days per year assumption. It is used to calculate Compound Annual Growth Rate (CAGR). Default value is 252 trading days per year.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis

示例

ax = rp.plot_table(returns=Y, w=w1, MAR=0, alpha=0.05, ax=None)

- PlotFunctions.plot_clusters(returns, custom_cov=None, codependence='pearson', linkage='ward', k=None, max_k=10, bins_info='KN', alpha_tail=0.05, gs_threshold=0.5, leaf_order=True, show_clusters=True, dendrogram=True, cmap='RdYlBu', linecolor='fuchsia', title='', height=12, width=12, ax=None)[源代码]

Create a clustermap plot based on the selected codependence measure.

- 参数:

returns (DataFrame) – Assets returns.

custom_cov (DataFrame or None, optional) – Custom covariance matrix, used when codependence parameter has value ‘custom_cov’. The default is None.

codependence (str, can be {'pearson', 'spearman', 'abs_pearson', 'abs_spearman', 'distance', 'mutual_info', 'tail' or 'custom_cov'}) –

The codependence or similarity matrix used to build the distance metric and clusters. The default is ‘pearson’. Possible values are:

’pearson’: pearson correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho_{i,j})}\).

’spearman’: spearman correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho_{i,j})}\).

’kendall’: kendall correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{kendall}_{i,j})}\).

’gerber1’: Gerber statistic 1 correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{gerber1}_{i,j})}\).

’gerber2’: Gerber statistic 2 correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{gerber2}_{i,j})}\).

’abs_pearson’: absolute value pearson correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho_{i,j}|)}\).

’abs_spearman’: absolute value spearman correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho_{i,j}|)}\).

’abs_kendall’: absolute value kendall correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho^{kendall}_{i,j}|)}\).

’distance’: distance correlation matrix. Distance formula \(D_{i,j} = \sqrt{(1-|\rho_{i,j}|)}\).

’mutual_info’: mutual information matrix. Distance used is variation information matrix.

’tail’: lower tail dependence index matrix. Dissimilarity formula \(D_{i,j} = -\log{\lambda_{i,j}}\).

’custom_cov’: use custom correlation matrix based on the custom_cov parameter. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{pearson}_{i,j})}\).

linkage (string, optional) –

Linkage method of hierarchical clustering, see linkage for more details. The default is ‘ward’. Possible values are:

’single’.

’complete’.

’average’.

’weighted’.

’centroid’.

’median’.

’ward’.

’DBHT’: Direct Bubble Hierarchical Tree.

k (int, optional) – Number of clusters. This value is took instead of the optimal number of clusters calculated with the two difference gap statistic. The default is None.

max_k (int, optional) – Max number of clusters used by the two difference gap statistic to find the optimal number of clusters. The default is 10.

Number of bins used to calculate variation of information. The default value is ‘KN’. Possible values are:

’KN’: Knuth’s choice method. See more in knuth_bin_width.

’FD’: Freedman–Diaconis’ choice method. See more in freedman_bin_width.

’SC’: Scotts’ choice method. See more in scott_bin_width.

’HGR’: Hacine-Gharbi and Ravier’ choice method.

int: integer value choice by user.

alpha_tail (float, optional) – Significance level for lower tail dependence index. The default is 0.05.

gs_threshold (float, optional) – Gerber statistic threshold. The default is 0.5.

leaf_order (bool, optional) – Indicates if the cluster are ordered so that the distance between successive leaves is minimal. The default is True.

show_clusters (bool, optional) – Indicates if clusters are plot. The default is True.

dendrogram (bool, optional) – Indicates if the plot has or not a dendrogram. The default is True.

cmap (str or cmap, optional) – Colormap used to plot the pcolormesh plot. The default is ‘viridis’.

linecolor (str, optional) – Color used to identify the clusters in the pcolormesh plot. The default is fuchsia’.

title (str, optional) – Title of the chart. The default is “”.

height (float, optional) – Height of the image in inches. The default is 12.

width (float, optional) – Width of the image in inches. The default is 12.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis

示例

ax = rp.plot_clusters(returns=Y, codependence='spearman', linkage='ward', k=None, max_k=10, leaf_order=True, dendrogram=True, ax=None)

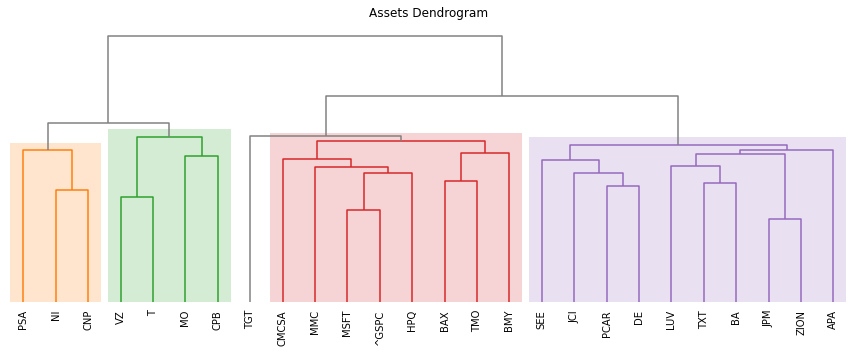

- PlotFunctions.plot_dendrogram(returns, custom_cov=None, codependence='pearson', linkage='ward', k=None, max_k=10, bins_info='KN', alpha_tail=0.05, gs_threshold=0.5, leaf_order=True, show_clusters=True, title='', height=5, width=12, ax=None)[源代码]

Create a dendrogram based on the selected codependence measure.

- 参数:

returns (DataFrame) – Assets returns.

custom_cov (DataFrame or None, optional) – Custom covariance matrix, used when codependence parameter has value ‘custom_cov’. The default is None.

codependence (str, can be {'pearson', 'spearman', 'abs_pearson', 'abs_spearman', 'distance', 'mutual_info', 'tail' or 'custom_cov'}) –

The codependence or similarity matrix used to build the distance metric and clusters. The default is ‘pearson’. Possible values are:

’pearson’: pearson correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho_{i,j})}\).

’spearman’: spearman correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho_{i,j})}\).

’kendall’: kendall correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{kendall}_{i,j})}\).

’gerber1’: Gerber statistic 1 correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{gerber1}_{i,j})}\).

’gerber2’: Gerber statistic 2 correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{gerber2}_{i,j})}\).

’abs_pearson’: absolute value pearson correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho_{i,j}|)}\).

’abs_spearman’: absolute value spearman correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho_{i,j}|)}\).

’abs_kendall’: absolute value kendall correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho^{kendall}_{i,j}|)}\).

’distance’: distance correlation matrix. Distance formula \(D_{i,j} = \sqrt{(1-|\rho_{i,j}|)}\).

’mutual_info’: mutual information matrix. Distance used is variation information matrix.

’tail’: lower tail dependence index matrix. Dissimilarity formula \(D_{i,j} = -\log{\lambda_{i,j}}\).

’custom_cov’: use custom correlation matrix based on the custom_cov parameter. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{pearson}_{i,j})}\).

linkage (string, optional) –

Linkage method of hierarchical clustering, see linkage for more details. The default is ‘ward’. Possible values are:

’single’.

’complete’.

’average’.

’weighted’.

’centroid’.

’median’.

’ward’.

’DBHT’: Direct Bubble Hierarchical Tree.

k (int, optional) – Number of clusters. This value is took instead of the optimal number of clusters calculated with the two difference gap statistic. The default is None.

max_k (int, optional) – Max number of clusters used by the two difference gap statistic to find the optimal number of clusters. The default is 10.

Number of bins used to calculate variation of information. The default value is ‘KN’. Possible values are:

’KN’: Knuth’s choice method. See more in knuth_bin_width.

’FD’: Freedman–Diaconis’ choice method. See more in freedman_bin_width.

’SC’: Scotts’ choice method. See more in scott_bin_width.

’HGR’: Hacine-Gharbi and Ravier’ choice method.

int: integer value choice by user.

alpha_tail (float, optional) – Significance level for lower tail dependence index. The default is 0.05.

gs_threshold (float, optional) – Gerber statistic threshold. The default is 0.5.

leaf_order (bool, optional) – Indicates if the cluster are ordered so that the distance between successive leaves is minimal. The default is True.

show_clusters (bool, optional) – Indicates if clusters are plot. The default is True.

title (str, optional) – Title of the chart. The default is “”.

height (float, optional) – Height of the image in inches. The default is 5.

width (float, optional) – Width of the image in inches. The default is 12.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis

示例

ax = rp.plot_dendrogram(returns=Y, codependence='spearman', linkage='ward', k=None, max_k=10, leaf_order=True, ax=None)

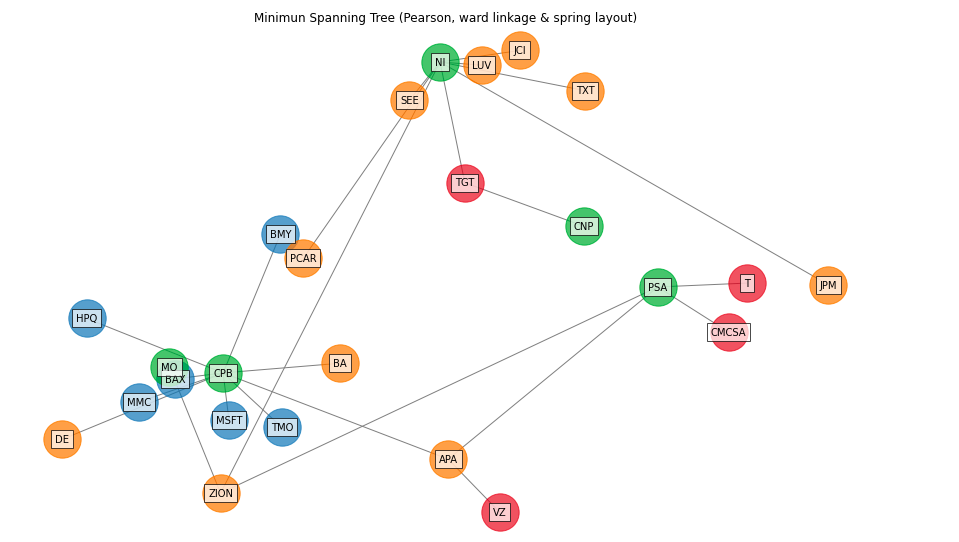

- PlotFunctions.plot_network(returns, custom_cov=None, codependence='pearson', linkage='ward', k=None, max_k=10, bins_info='KN', alpha_tail=0.05, gs_threshold=0.5, leaf_order=True, kind='spring', seed=0, node_labels=True, node_size=1400, node_alpha=0.7, font_size=10, title='', height=8, width=10, ax=None)[源代码]

Create a network plot. The Planar Maximally Filtered Graph (PMFG) for DBHT linkage and Minimum Spanning Tree (MST) for other linkage methods.

- 参数:

returns (DataFrame) – Assets returns.

custom_cov (DataFrame or None, optional) – Custom covariance matrix, used when codependence parameter has value ‘custom_cov’. The default is None.

codependence (str, can be {'pearson', 'spearman', 'abs_pearson', 'abs_spearman', 'distance', 'mutual_info', 'tail' or 'custom_cov'}) –

The codependence or similarity matrix used to build the distance metric and clusters. The default is ‘pearson’. Possible values are:

’pearson’: pearson correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{pearson}_{i,j})}\).

’spearman’: spearman correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{spearman}_{i,j})}\).

’kendall’: kendall correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{kendall}_{i,j})}\).

’gerber1’: Gerber statistic 1 correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{gerber1}_{i,j})}\).

’gerber2’: Gerber statistic 2 correlation matrix. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{gerber2}_{i,j})}\).

’abs_pearson’: absolute value pearson correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho_{i,j}|)}\).

’abs_spearman’: absolute value spearman correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho_{i,j}|)}\).

’abs_kendall’: absolute value kendall correlation matrix. Distance formula: \(D_{i,j} = \sqrt{(1-|\rho^{kendall}_{i,j}|)}\).

’distance’: distance correlation matrix. Distance formula \(D_{i,j} = \sqrt{(1-\rho^{distance}_{i,j})}\).

’mutual_info’: mutual information matrix. Distance used is variation information matrix.

’tail’: lower tail dependence index matrix. Dissimilarity formula \(D_{i,j} = -\log{\lambda_{i,j}}\).

’custom_cov’: use custom correlation matrix based on the custom_cov parameter. Distance formula: \(D_{i,j} = \sqrt{0.5(1-\rho^{pearson}_{i,j})}\).

linkage (string, optional) –

Linkage method of hierarchical clustering, see linkage for more details. The default is ‘ward’. Possible values are:

’single’.

’complete’.

’average’.

’weighted’.

’centroid’.

’median’.

’ward’.

’DBHT’: Direct Bubble Hierarchical Tree.

k (int, optional) – Number of clusters. This value is took instead of the optimal number of clusters calculated with the two difference gap statistic. The default is None.

max_k (int, optional) – Max number of clusters used by the two difference gap statistic to find the optimal number of clusters. The default is 10.

Number of bins used to calculate variation of information. The default value is ‘KN’. Possible values are:

’KN’: Knuth’s choice method. See more in knuth_bin_width.

’FD’: Freedman–Diaconis’ choice method. See more in freedman_bin_width.

’SC’: Scotts’ choice method. See more in scott_bin_width.

’HGR’: Hacine-Gharbi and Ravier’ choice method.

int: integer value choice by user.

alpha_tail (float, optional) – Significance level for lower tail dependence index. The default is 0.05.

gs_threshold (float, optional) – Gerber statistic threshold. The default is 0.5.

leaf_order (bool, optional) – Indicates if the cluster are ordered so that the distance between successive leaves is minimal. The default is True.

kind (str, optional) –

Kind of networkx layout. The default value is ‘spring’. Possible values are:

’spring’: networkx spring_layout.

’planar’. networkx planar_layout.

’circular’. networkx circular_layout.

’kamada’. networkx kamada_kawai_layout. Only available for positive codependence metrics. Not pearson or spearman except when linkage is DBHT.

seed (int, optional) – Seed for networkx spring layout. The default value is 0.

node_labels (bool, optional) – Specify if node lables are visible. The default value is True.

node_size (float, optional) – Size of the nodes. The default value is 1600.

node_alpha (float, optional) – Alpha parameter or transparency of nodes. The default value is 0.7.

font_size (float, optional) – Font size of node labels. The default value is 12.

title (str, optional) – Title of the chart. The default is “”.

height (float, optional) – Height of the image in inches. The default is 5.

width (float, optional) – Width of the image in inches. The default is 12.

ax (matplotlib axis, optional) – If provided, plot on this axis. The default is None.

- 抛出:

ValueError – When the value cannot be calculated.

- 返回:

ax – Returns the Axes object with the plot for further tweaking.

- 返回类型:

matplotlib axis

示例

ax = rp.plot_network(returns=Y, codependence="pearson", linkage="ward", k=None, max_k=10, alpha_tail=0.05, leaf_order=True, kind='spring', ax=None)